DePuy Maryland Case Off, On to California

January 10, 2012 – The lawsuit against artificial hip manufacturer DePuy Orthopaedics (Moira Jackson v. DePuy Orthopaedics) scheduled for trial in Prince George’s County, Maryland this past week ended when the plaintiff dropped her lawsuit just after jury selection was concluded according to Bloomberg.

January 10, 2012 – The lawsuit against artificial hip manufacturer DePuy Orthopaedics (Moira Jackson v. DePuy Orthopaedics) scheduled for trial in Prince George’s County, Maryland this past week ended when the plaintiff dropped her lawsuit just after jury selection was concluded according to Bloomberg.

According to some web reports which have yet to be confirmed, she may refile to pursue remedy in federal court.

Later this month, a California lawsuit is expected to commence trial pending the results of a defense motion for summary judgment, filed last November, scheduled to be heard tomorrow.

Plaintiffs who may be anticipating settlements stemming from the DePuy litigation are encouraged to familiarize themselves with the concept structured settlements as an option for receiving any compensation they may be entitled to.

For further information, please visit:

We welcome the opportunity to be of service and urge all clients pursuing legal remedy to educate themselves on the income tax-free benefits of structured settlements for their injury claims.

Posted: January 11, 2013 | Category: Articles, Blog, DePuy ASR Hip Recall, Structured Settlements | Comments Off on DePuy Maryland Case Off, On to California

When A Tax Attacks

Tax Deal Could Bring Unwelcome Surprises

January 7, 2013 – While those earning less than $400,000 ($450,000 for married couples) may be breathing a collective sigh of relief because Congress made their tax brackets “permanent” on New Year’s Day, a little digging reveals that maybe they shouldn’t sigh too deeply.

Not just yet anyway.

According to today’s Fortune article published in CNNMoney, there is good reason to be a little more concerned about your taxable income than first meets the eye.

For starters, the Alternative Minimum Tax (AMT) phaseout included in the recent tax deal potentially increases some taxpayers’ income by several percentage points even though their brackets remained intact.

For starters, the Alternative Minimum Tax (AMT) phaseout included in the recent tax deal potentially increases some taxpayers’ income by several percentage points even though their brackets remained intact.

Don’t worry if you’re not completely sure what AMT is all about. Your accountant surely does.

The article cautions that those making between $150,000 and $473,200 might want to start doing some early tax planning for 2013 because they could be impacted.

Fortunately for contingency fee plaintiff attorneys and individuals anticipating a settlement from a personal, non-physical (i.e. taxable) injury lawsuit, we offer a solution.

Anticipating something like this might happen, a few months ago we published a webinar entitled Structuring Your Taxable Settlements to demonstrate the value of tax deferral for those who qualify. We even created a special website designed to highlight the problem and to help you make a more informed decision about your financial future. Be sure to visit:

It’s not always easy and it’s rarely fun. But investing the time to plan for saving money is always time well spent.

Posted: January 7, 2013 | Category: Articles, Blog, Structured Settlements | Comments Off on When A Tax Attacks

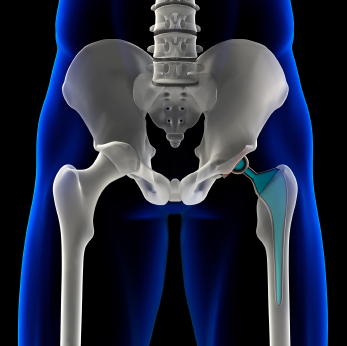

First DePuy Trial To Begin

January 4, 2013 – According to various sources, the first state trial in the United States involving the much maligned DePuy ASR artificial hip is scheduled to go out on Monday, January 7, 2013 in Prince George County, Maryland.

While industry insiders will be watching this state trial with great interest, more interest will likely be paid to the first federal trials stemming from the lawsuits consolidated in the Ohio multidistrict litigation against DePuy directly.

Two trials are tentatively scheduled for May 6, 2013 and July 8, 2013.

Those involved in any litigation stemming from the DePuy ASR litigation are invited to visit our firm’s companion site, ASRHipSettlement.com, to learn more about how they may benefit from choosing a structured settlement for all or part of any post-settlement proceeds they may be awarded.

Posted: January 4, 2013 | Category: Articles, Blog, DePuy ASR Hip Recall, Structured Settlements | Tags: DePuy, structured settlement | Comments Off on First DePuy Trial To Begin

Many Cars Flunk Safety Test

December 20, 2012 – While car safety has generally improved in recent years, a new, more specific, crash test designed and administered by the Insurance Institute for Highway Safety (IIHS), revealed that eight of eleven luxury and near luxury cars weren’t up to the challenge.

They flunked the test.

This new test, which replicates certain front end collisions, was created in part to help stave off the 10,000 plus deaths which still occur every year despite the auto industry’s ongoing efforts to improve vehicle safety.

When automobile accidents result in serious injury or death, we are typically called upon to assist the survivors with structured settlement choices designed to help them put their lives back in order where injury compensation proceeds are concerned.

While we pride ourselves on our ability to help clients with their post-accident settlement planning, we hope you never require our services because of an auto accident you or your loved ones are involved in.

And if you are in the market for a new car, it may be worth your time to review these crash results before making your selection.

Wishing you an accident-free holiday season and safe driving in 2013 and beyond!

Posted: December 20, 2012 | Category: Articles, Blog, Structured Settlements | Comments Off on Many Cars Flunk Safety Test

Best Defense Against Defense Contractor Award

88% of $7.1 Million Award Attributed to Punitive Damages

November 3, 2012 – Defense contractor KBR was recently found negligent by an Oregon jury for “knowingly” exposing National Guard soldiers to toxic chemicals while they were serving their country in Iraq according to CNN.

Each plaintiff was awarded $850,000 in non-economic damages and $6.25 Million in punitive damages in the $85 Million judgment.

Practice Pointer: Although a defense appeal is planned, the plaintiff soldiers are urged to consider the tax implications of this settlement NOW in the event a post-judgment settlement is negotiated.

Because the punitive component is fully taxable, utilizing a Non-Physical Injury Structured Settlement for this portion of the settlement holds tremendous potential to help mitigate the tax impact of such an award.

Our firm recently hosted a webinar on this very topic which explains the impact in detail.

To increase the chances for long-term financial security with a structured settlement following ANY judgment, clients are urged to analyze the tax consequences before accepting their verdict. Proper planning can have a positive impact on the ultimate recovery and help plaintiffs keep as much of their award as possible.

Posted: November 3, 2012 | Category: Articles, Blog, Structured Settlements | Comments Off on Best Defense Against Defense Contractor Award

Money Talks

And it usually says, “Spend me, spend me, spend me!”

This is one of the underlying fears of extremely wealthy people who fret about leaving too much money to their heirs.

People unaccustomed to handling large sums of money often end up in a dark place and/or are easy targets for others seeking to separate them from their sudden riches.

As California family law attorney and prolific blogger Mark Brian Baer highlighted in a recent post, the family of Whitney Houston recognizes this risk and is fighting to change the terms of Houston’s daughter’s $20 Million inheritance.

While most personal injury settlements resolve for significantly less than these kinds of dollars, the same risk is nonetheless omnipresent.

For this reason alone, choosing a structured settlement for some portion of one’s personal injury claim makes all the sense in the world.

Often, the argument is made that “rates are too low for me/my client to consider structuring.”

But for anyone who can relate to the temptation brought on by the infamous talking money, it may be worth re-prioritizing the superior value of delayed gratification over speculative returns.

Returns which, if readily available cash is spent too quickly, may never materialize anyway.

Thomas Jefferson’s advice to “never put off till tomorrow what you can do today” might make sense for daily chores.

But when it comes to money, “putting off till tomorrow what you can spend today” may just lead to a happier, more secure place.

Posted: October 31, 2012 | Category: Articles, Blog, Structured Settlements | Comments Off on Money Talks

The Good Old Days

When my great-great-grandfather, Patrick Finn, arrived in Winsted, Connecticut as a young lad from County Cork, Ireland in the mid-1850s, he couldn’t have had any kind of future planned for himself yet.

How could he? He was only four years old.

But by the time he was a teenager, young Patrick successfully landed a good job with the Empire Knife Company where he began honing (pun intended) his craft in the cutlery trade.

Probably glad to have any job given the prejudice which existed at the time.

At least I assume g-g-grandpa Finn found himself a good job.

After all, he worked there for about 60 years. Right up until age 77, just a few scant years before he died.

Blast To The Past

Fast forward almost a century and it turns out that maybe those long, hard “work ’til you’re almost dead because you have to” expectations aren’t such a thing of the past anymore.

In fact, maybe our forefathers had it made.

Post-Great Recession retirement planning, it turns out, has changed fairly dramatically according to Blake Ellis in his October 23, 2012 column for CNNMoney.

In his article “More Americans delaying retirement until their 80s,” we learn that retirement may look a lot different than many of us planned when we jumped into the labor force.

Fortunately for those anticipating a personal injury settlement, a unique opportunity exists to help fend off this retirement killjoy.

Structured settlements allow an individual to choose, in advance of settlement, to arrange for their settlement proceeds to be paid out in future years on a tax-advantaged basis.

Personal, physical injury settlements are paid 100% income tax-free while certain personal, non-physical injury settlements can be concluded on a tax-deferred basis.

Either way, the potential for enhanced retirement security is very possible.

We don’t think people should sue someone just to boost their chances for retirement bliss.

But for those of you who happen to be in the throes of settling a personal injury claim, a structured settlement may hold the key to providing you with the future you once dreamed of.

And deserve.

Posted: October 30, 2012 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on The Good Old Days

A Happier Retirement

Managing the Risks – A Delicate Balance

Achieving a happy, comfortable retirement is largely dependent upon how successful one is at managing the many retirement risks we all face leading up to, and during, retirement.

Depending on whose literature you read there are anywhere from six to ten or more risks people should consider when planning for their post-working life lives.

Over the years, we’ve spent a lot of time talking about the consensus greatest risk everyone faces in retirement: Living too long!

- Because life expectancies are merely averages, basing your retirement planning (and spending decisions) on your statistical life expectancy, in an era when many people live well into their nineties, can lead to the very unhappy reality that your nest egg will predecease you. And we think dying broke is one very scary proposition!

But in addition to this longevity risk, we want to introduce you to another concept you may not have heard much about but which can be just as detrimental to your retirement happiness if not considered: Behavioral risk.

Behavioral risk is the risk of human biases getting in the way of sound decision making as it pertains to retirement planning.

Both longevity risk and behavioral risk, along with several others, are covered quite concisely in “Quantifying Key Risks in Retirement” produced by the Institutional Retirement Income Council.

Increasing Your Retirement Happiness

So you’ve successfully considered all the retirement risks you face and are now ready to take action. What is the best way to achieve retirement bliss?

In our view, three words:

ANNUITIES . . . ANNUITIES . . . ANNUITIES

It seems an over-simplification but the more you look at annuities, the more you’re likely to realize how effectively they address so many retirement needs.

But don’t just take our word for it. Here’s what Meir Statman, Professor of Finance at the Leavey School of Business, Santa Clara University has to say on the subject in a recent article which appears in Annuity Digest entitled “Meir Statman on the Behavioral Obstacles Affecting Investing and Retirement Planning” (emphasis added):

“People who know they have a pension or annuity income coming every month have more than utilitarian well-being, they also have psychological well-being. People with pensions, annuities or other guaranteed income are happier in retirement and show fewer symptoms of depression than people with equal income from sources which are not as assured.”

– Meir Statman –

Such a growing body of research links happiness to having secure, guaranteed cash flow that we continue to recommend them for anyone facing retirement or anticipating a personal injury settlement.

So be happy. Choose the annuity!

Posted: September 20, 2012 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on A Happier Retirement

Structured Settlements: Bonding Your Future

Adjusting Your Expectations in a Post-Economic Meltdown World

If you were fortunate enough to have invested in stocks over the past 30 or so years; and,

If you were fortunate enough to have stayed with it through the past four years when the financial world went crazy; and,

If you still have a good portion of what you’ve managed to sock away; then,

At the risk of over-stating the obvious, you are indeed fortunate.

But that was, as The Monkees once sang, then. This is now.

Stock-Bond Return Gap Should Narrow

MONEY Senior Editor Walter Updegrave lays out a pretty good case for why folks may want to temper their expectations about future market returns in his article “The case for investing in bonds, too.”

Back “then” stock returns significantly outperformed bonds.

But “now” the rate of return gap between the two is predicted to be much narrower according to a number of experts. This means bonds might still make a good deal of sense despite their current perceived “low” rate of return.

Even Better for Structured Settlements

Structured settlements, which are backed by portfolios consisting largely of bonds, offer superior financial security and, because benefits are paid out 100% income tax-free, they remain an excellent choice for those seeking safety and security.

And because of their decided tax advantage (principal AND interest are paid 100% income-tax free), returns can be commensurate with the after-tax, after-fee stock market returns.

Minus the risk.

Nobody knows for sure what the future holds. But we know the wild run-ups stocks enjoyed during much of the 80s/90s were pretty exceptional by historical standards. So choosing a structured settlement is still a wise choice for those who want to secure their own financial future.

Posted: September 19, 2012 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on Structured Settlements: Bonding Your Future

Pension Choices

Lifetime Income or Lump Sum?

There’s no such thing as a one-size-fits-all when it comes to making decisions about your retirement options.

But choosing lifetime income instead of a lump sum for your pension distribution makes tremendous sense for a variety of reasons.

The simple truth is . . .

“Nothing provides you with a statistically better chance that you will have guaranteed income you can never outlive.”

In his recent MONEY column “Your Pension: Lump sum vs. monthly payments,” senior editor Walter Updegrave compares the two choices and points out how difficult it can be to outperform the lifetime income option when you choose a lump sum distribution.

The article includes a telling graph which illustrates how dramatically your chances of running out of money increase as you age.

IF you take the lump sum, that is.

This risk of running out of money decreases to zero if you choose the monthly income option.

For those anticipating a personal injury settlement, the additional tax benefits can make the lifetime income option even MORE attractive.

Make your money last.

Sleep better at night.

We can’t guarantee a lifetime income option is best for you. But we can give you the information you need so you can decide what’s best for YOU!

Posted: August 29, 2012 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on Pension Choices