The Dawning of the Age of Annuities

May 2, 2013 – When HAIR: The American Tribal Love-Rock Musical debuted at The Public Theater in 1967 as the venue’s first-ever production, our country’s social fabric was in the midst of a rinse cycle involving some pretty harsh chemicals.

May 2, 2013 – When HAIR: The American Tribal Love-Rock Musical debuted at The Public Theater in 1967 as the venue’s first-ever production, our country’s social fabric was in the midst of a rinse cycle involving some pretty harsh chemicals.

Literally and figuratively.

Just twelve years earlier, the most popular album of the time was Frank Sinatra’s In The Wee Small Hours.

By 1967, it was Sgt. Pepper’s Lonely Hearts Club Band.

Yes, the world was changing. People were rejecting the values of those who preceded them. Sacred cows were no longer sacrosanct and established norms were feeling nearly as faded as Bobby McGee’s lover’s jeans.

This was the Dawning of the Age of Aquarius we would soon learn.

Annuities/(Let The Sunshine In)

Fast forward forty-six years and a similar rejection of what’s always passed as conventional wisdom is afoot when it comes to retirement planning.

More specifically, as Sheyna Steiner, writing for bankrate.com asks rhetorically in her weblog “Retiring on CDs Not Viable,”

“Is this (the dawning of) the age of annuities?”

And she’s not talking about compact discs, by the way.

The old rule of thumb that any retiree could choose a sensible mix of stocks and bonds and/or other securities, “draw down” their retirement nest egg 4% each year and have enough money to live on for the rest of their life no longer holds up to scrutiny in a post-Great Recession world.

Side Bar: We were ahead of this trend! For a link to one of our earlier posts on this very same topic, be sure to check out:

July 4, 2011: A Paycheck for Life

In fact, sticking with this previous generation’s establish formula could easily lead to financial ruin and even poverty tarnishing those Golden Years you worked so hard to achieve.

The failure rate for this draw down approach, or the probability of running completely out of money while you’re still alive, is estimated to be as high as 57%.

Life annuities, on the other hand, solve this problem for retirees and soon-to-be-retirees.

As we’ve advocated for years, annuities help people sleep better at night since they know the annuity will keep paying as long as they live. The highs and lows of market conditions do not impact guaranteed cash flows offered by annuities. Like a pension, you know exactly what you’re going to receive each month for as long as you live.

Structured settlement annuities, for those who are able to take advantage of them, can be even better and offer unique advantages unavailable to the general public.

But for the vast majority of Americans with 401(k) balances or other savings looking to secure their future as sensibly and cost effectively as possible, nothing can replace the peace of mind that comes with knowing that periodic payments, guaranteed by a highly rated life insurance carrier, will be there whether you live to age 75, 85, 95 or beyond.

If you were lucky enough to dodge the 2008-2009 stock market bullet, don’t take chances this time around. Convert a portion of your nest egg to a life annuity to secure your future. We have lots of choices available to you.

So call us TODAY for a quote so we can help you align your retirement Jupiter with your life expectancy Mars.

Then, all you gotta do is let the sunshine in!

Posted: May 2, 2013 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on The Dawning of the Age of Annuities

Thank You, Senator Baucus!

April 23, 2013 – Today’s announcement that Sen. Max Baucus (D-MT) will NOT be seeking a seventh term is indeed a “mixed emotions” news item for the structured settlements community.

While we all wish our industry’s long time friend the absolute best life has to offer as he retires to the magnificent Big Sky country he calls home, his departure leaves a void that will be deeply felt.

“Our industry will miss you, Mr. Chairman.”

As Chairman of the powerful Senate Finance Committee, Sen. Baucus has continued to fight for the rights of accident victims.

He was an original sponsor of the tax rules that Congress enacted in 1982 which paved the way for more widespread use of the then-still evolving claims negotiation, resolution and settlement technique known as “structured settlements.”

It is because of Sen. Baucus’ ongoing commitment to the long-term well-being of those who are anticipating settlements for personal, physical injury claims that these laws exist today.

In addition to the original tax laws, Sen. Baucus was always at the forefront of other important pieces of structured settlement-related legislation. Among those to make their way into the law of the land were:

Taxpayer Relief Act of 1997

Victims of Terrorism Tax Relief Act of 2001

It might be fitting to someday create a Mt. Rushmore-like sculpture to honor those dedicated Americans who made structured settlements possible. If and when that day comes, surely the mountain will be in Montana and Sen. Max Baucus its most prominent figure.

Until then, I feel comfortable in speaking for the entire structured settlements community in saying,

“Thank you, Sen. Baucus, for more than thirty years of dedicated service to the structured settlements industry. We appreciate everything you’ve done for so many.”

You will be missed.

But never forgotten.

Posted: April 23, 2013 | Category: Articles, Blog, Structured Settlements | Comments Off on Thank You, Senator Baucus!

Young and Not-So-Foolish After All

April 22, 2013 – With all apologies to Dean Martin, Tony Bennett and anyone else who ever crooned the old Hague/Horwit standard, it turns out “young” folks aren’t so foolish after all.

At least not when it comes to making financial decisions if you believe two recent articles published in InvestmentNews.

At least not when it comes to making financial decisions if you believe two recent articles published in InvestmentNews.

The first article, “Throw caution to the wind? Not young boomers,” features a study by Allianz Life Insurance Co. of North America which concludes that younger baby boomers are significantly more willing to accept lower returns in exchange for reduction or elimination of downside market risk.

Among the highlights of this study:

87% of respondents would prefer a 4% return with zero chance of loss to something offering an 8% return with a possibility of market loss

Among women, the preference for risk aversion was even higher with 91% preferring the 4%/no loss combination

It shouldn’t come as a surprise then that indexed and income annuity sales hit record levels last year topping $43.4 billion.

The second InvestmentNews article goes even younger. “NY Life cuts initial deposit for annuity to attract youth” announces the life company’s decision to cultivate clients from among the sub-boomer population by reducing its minimum initial deposit to $5,000 from $10,000.

New York Life is one of the most admired companies in the world and is also very active in the structured settlement and structured attorney fee market: two of our firm’s core specialties.

Neither of these trends surprise us.

Neither of these trends surprise us.

If you’ve been a regular subscriber, you may recall an article we published in our newsletter two years ago this month entitled “Young Workers: Make Mine Guaranteed.”

That piece highlighted a Towers Watson survey of younger employees and the value they placed on guaranteed income.

We’re proud to have been a few years ahead of the trend on that one.

Bottom Lining It For You:

People generally want safety and security. Even if it means forfeiting higher potential returns, people across all age and income brackets are choosing the tortoise over the hare to meet basic retirement needs.

You’re never too young or too old to be smart with your money. After all, it’s yours. Why not hold onto it and put it to work for you.

Posted: April 22, 2013 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on Young and Not-So-Foolish After All

Structured Settlements in Claims

April 8, 2013 – Things were so different in 1983 when I began my claims career than they are today.

Notices of loss were still being taken by hand.

Notices of loss were still being taken by hand.

Pretty much every claims manager had his own secretary. (And I used “his” intentionally since nearly every claims manager was male)

Among the tools in common usage today which had yet to be invented: The Internet, personal computers, cell phones, GPS and filmless cameras.

That same year, H. R. 5470, The Periodic Payment Settlement Act of 1982, as passed by the United States Congress’ Joint Committee on Taxation, went into effect ushering in an era of widespread use of a concept that had been brewing in the claims world for a number of years:

Back then, management span of control was narrower, claims training more prevalent and it was unheard of for someone to work from home. Even field adjusters reported to an office to receive their assignments (by hand) from their supervisor.

During these and the years that followed, as this new “structured settlement” concept grew, claims departments began embracing their usage as a creative solution to resolving injury disputes. Carriers developed their own structured settlement programs and in those high interest, high inflation years, structured settlements helped many an unsettleable claim, settle.

Fast forward to 2013.

Claims training is less prominent than it used to be.

Seemingly every day, greater demands are placed on claims professionals.

And fewer claims people understand the nuances of structured settlements.

Which made reading this month’s Claims magazine article, “The Perks of Structured Settlements: Faster Claims Closure At The Right Price” so compelling.

Bylined by respected veteran claims executive Brian N. Farrell, the article does a great job going “back to the basics” highlighting some of the overlooked reasons why claims departments should continue to embrace the use of structured settlements as a claims resolution tool in today’s economy.

In addition to the obvious benefits to the injured parties which are well documented, the author emphasizes the benefits of using structured settlements to establish proper reserves, control litigation costs and ensure good faith bargaining among other ancillary reasons.

It’s a good read and a timely reminder that structured settlements remain one of the best kept secrets in the insurance world.

Unlike other claims tools which have been replaced by bigger, better and faster alternatives, structured settlements have yet to be improved upon and more carriers would be well served by rededicating themselves to expanding their use.

Posted: April 8, 2013 | Category: Articles, Blog, Structured Settlements | Comments Off on Structured Settlements in Claims

Say Hello to Collaborative Courts Foundation of Orange County’s Newest Board Member

Dan Finn joins CCFOC Board of Directors

March 29, 2013 – The Collaborative Courts Foundation of Orange County (CCFOC) recently invited me to join its distinguished Board of Directors.

I was only too honored to enthusiastically accept the opportunity to become part of an organization that positively impacts the lives of so many people while playing such a vital role in Orange County’s civil justice system.

I was only too honored to enthusiastically accept the opportunity to become part of an organization that positively impacts the lives of so many people while playing such a vital role in Orange County’s civil justice system.

Last week, at its monthly meeting, the CCFOC Board made it official by voting me in as its newest member.

It’s a great honor to continue my commitment to community service in this capacity.

As if to prove that “when one (board) door closes, another opens,” this invitation comes just as my four year commitment as a board member of the National Structured Settlements Trade Association (NSSTA) draws to a close.

My term as NSSTA’s Immediate Past President officially ends April 19.

CCFOC exists to support the efforts of the Superior Court of California, County of Orange’s Collaborative Court initiative. As described on Orange County Superior Court’s website:

“Collaborative or “problem solving” Courts are specialized court tracks that address underlying issues that may be present in the lives of persons who come before the court on criminal, juvenile, or dependency matters. These life-changing programs involve active judicial monitoring and a team approach to decision making, and include the participation of a variety of different agencies, such as Probation and health treatment providers.”

Committed to fostering “therapeutic justice,” the foundation’s mission is to provide support & services to participants in the Orange County Collaborative Court programs, so they will overcome obstacles and become productive members of society.

Please visit CCFOC’s website for a description of the programs and services we provide.

If you, your companies or law firms are interested in helping to support our efforts, we welcome your assistance as a donor, sponsor or supporter. Since CCFOC is a 503(c)(3) nonprofit corporation, your contributions are tax deductible to the fullest extent of the law.

And if you live in Orange County, mark your calendars for Saturday, September 7 and plan to join us for our third annual fundraiser dinner being held at Seven Degrees in Laguna Beach.

Thank you to my fellow board members for your vote of confidence in me. I look forward to serving with you and want to again publicly profess how honored I am to be part of the Collaborative Courts Foundation of Orange County.

Let’s do some good!

Posted: March 29, 2013 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on Say Hello to Collaborative Courts Foundation of Orange County’s Newest Board Member

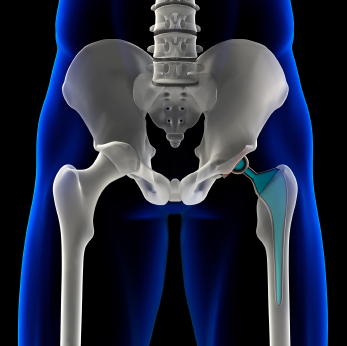

DePuy Deserves Blame for Failed Hips

March 25, 2013 – That’s the conclusion of the USA Today Editorial Board following its analysis of the recently concluded Los Angeles Kransky v DePuy trial in which a jury found the device manufacturer negligent to the tune of $8.3 million in compensatory damages awarded to a retired Montana prison guard who sued DePuy over complications arising from a failed metal-on-metal hip replacement.

The Kransky case, the first trial in the nation of approximately 10,000 lawsuits filed, is noteworthy for the higher than demanded compensatory value awarded and the finding that insufficient evidence existed to warrant punitive damages.

The Kransky case, the first trial in the nation of approximately 10,000 lawsuits filed, is noteworthy for the higher than demanded compensatory value awarded and the finding that insufficient evidence existed to warrant punitive damages.

The latter may change in future cases if USA Today‘s analysis is any indication.

The widely circulated daily newspaper contrasts DePuy’s slow response in recalling the defective ASR hip device from market once problems became known to Johnson & Johnson’s prompt response to the Tylenol cyanide poisoning cases nearly three decades earlier.

Johnson & Johnson is the parent company of DePuy Orthopaedics who manufactured the recalled devices.

The nation’s second defective DePuy hip lawsuit began in the Circuit Court of Cook County, Illinois just two weeks ago.

As all these case move forward, our firm remains committed to assisting those who have been adversely impacted. We have established a companion website, ASRHipSettlement,com, to help clients familiarize themselves with the benefits of resolving their disputes with DePuy by choosing a structured settlement.

We continue to monitor the DePuy litigation closely.

Posted: March 25, 2013 | Category: Articles, Blog, DePuy ASR Hip Recall, Structured Settlements | Comments Off on DePuy Deserves Blame for Failed Hips

Verdict: J&J was Negligent

March 8, 2013 – Jury deliberations have ended in the trial of Kransky v DePuy, the first lawsuit to go to trial in the United States for defective design of the recalled ASR metal-on-metal artificial hip manufactured by DePuy Orthopaedics, a division of Johnson & Johnson.

The verdict? Guilty of negligence.

The award: Mixed.

While the jury awarded the plaintiff, Loren “Bill” Kransky, $8.3 million (57% higher than demanded in closing arguments) in compensatory damages, they failed to attribute any punitive damages to the verdict according to Bloomberg.

Plaintiff attorneys had sought up to $179 million in punitive damages.

It remains to be seen what impact this verdict will have on the remaining 10,000+ cases awaiting trial but we will continue to watch this litigation closely.

Johnson & Johnson lawyers plan to appeal the jury’s verdict.

Posted: March 8, 2013 | Category: Articles, Blog, DePuy ASR Hip Recall, Structured Settlements | Comments Off on Verdict: J&J was Negligent

Annuities Hold the Key

March 7, 2013 – Shortly after posting an earlier blog on annuities today, I ran across an article I missed earlier in the week that reinforces the value of annuities in retirement planning.

Titled “Say Goodbye to the 4% Rule,” this Wall Street Journal column analyses a conventional retirement “draw down” strategy and comes to the conclusion that the rule is outdated. Instead, the author offers three alternatives.

The first alternative was music to our ears:

“Use annuities instead of bonds“

If you don’t want to read the entire piece, here’s an excerpt showing how annuities can hold the key to unlocking your retirement anxiety:

Pairing the most plain-vanilla type of annuity—called a single-premium immediate annuity—with stocks, retirees can generate income more safely and reliably than if they use bonds for that piece of their portfolio, says Wade Pfau, a professor who researches retirement income at the American College of Financial Services in Bryn Mawr, Pa

Pairing the most plain-vanilla type of annuity—called a single-premium immediate annuity—with stocks, retirees can generate income more safely and reliably than if they use bonds for that piece of their portfolio, says Wade Pfau, a professor who researches retirement income at the American College of Financial Services in Bryn Mawr, Pa

Did you catch that “more safely and reliably” part?

Safety and reliability is what we’re all about. So if you’re retired or soon to be retired and worried about securing your future, call us.

We can help.

We have access to a wide variety of the best single premium immediate annuities on the planet, along with other types to suit your risk tolerance, all certain to help you sleep better at night.

So call us. Buy an annuity that suits your needs. Then throw away the key!

Posted: March 8, 2013 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on Annuities Hold the Key

Annuities: 6 Questions

March 7, 2013 – All it takes is 2:20 to learn what questions you should ask before purchasing an annuity.

And that even includes the three seconds it takes to click on the video we posted here for you, produced by the Insurance Information Institute: “Buying an Annuity: 6 Questions to Ask”

And that even includes the three seconds it takes to click on the video we posted here for you, produced by the Insurance Information Institute: “Buying an Annuity: 6 Questions to Ask”

While there, spend some time learning about the powerful benefits of annuities.

We talk a lot about annuities because we believe in them.

We believe in them because they offer certainty that is difficult to replicate elsewhere without incurring additional risk.

If you do your own Google research on annuities, you’re likely to find conflicting recommendations about their usefulness in an overall financial or retirement plan.

“Financial advisers not associated with insurance companies will generally argue for putting little in annuities: they feel they can get better returns through a diversified portfolio of securities.

That’s a harder sell, though, after two rounds of huge losses in the stock market in one decade.”

Paul Sullivan, New York Times “Wealth Matters” Columnist

Investment losses later in life are even harder to make up because of the shorter time horizon.

Annuities Work

When you spend your adult life helping people secure their futures with annuities as I have, without a single complaint, you can’t possibly deny their value in one’s overall retirement strategy.

And when you add the tax benefits they afford, particularly on structured settlement annuities, you’d be hard pressed to find anything comparable.

We don’t say and will never say that annuities (at least the ones we offer) are the be-all and end-all of retirement choices. We believe in financial planners and managed funds and investment portfolios. Always have. Always will.

But as part of one’s overall retirement strategy, we can’t deny the value of adding a sure thing – annuities – to one’s future security.

Pensions, which have gone the way of the 8-track tape player, were good enough for previous generations.

Pension substitutes (aka annuities) are sensible replacements for this one.

Posted: March 7, 2013 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on Annuities: 6 Questions

Our “Best” Structured Settlement Endorsement Yet

With great pride we announce today our firm’s inclusion in Best’s Directory of Recommended Expert Service Providers in its Structured Settlement listing.

America’s premier independent insurance rating organization, A.M. Best Company, Inc. is designated as a Nationally Recognized Statistical Rating Organization (NRSRO) by the National Association of Insurance Commissioners (NAIC).

Directory listing eligibility is based upon an applicant’s “reputation, character and industry experience” and requires endorsements from past clients and peers familiar with the candidate’s credentials.

We are honored to be acknowledged as one of the nation’s only Structured Settlement Experts recognized by A.M. Best and are humbled by the outpouring of support received from the many attorneys, claims professionals and insurance industry veterans who gave so willingly of their time to validate our candidacy when contacted by this respected organization.

We share this distinction with all of you who make our success possible by trusting us with all your structured settlement and specialty annuity planning needs.

Thank you to everyone who participated in the vetting process and thank you all for continuing to believe in us. We appreciate the opportunity to be of service to YOU.

Best wishes for continued Struccess!

Posted: March 6, 2013 | Category: Articles, Blog, Newsletter, Retirement, Structured Sales, Structured Settlements | Comments Off on Our “Best” Structured Settlement Endorsement Yet