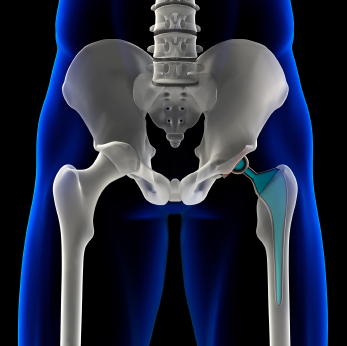

DePuy Exhibited “Bad Behavior”

This, according to Motley Fool contributor Sarah E. Wright in her column today entitled “4 Stocks Proving That Regulation Matters.”

Ms. Wright goes on to describe the 501(k) process which enables medical device manufacturers like DePuy to win approval for new products by simply claiming they are not materially different from existing approved devices.

As a result of the plethora of problems stemming from devices not properly tested, Congress has initiated work on a national surveillance strategy in an effort to protect consumers from defective products.

According to Forbes, the costs of claims associated with faulty hips like those produced by DePuy and other manufacturers is expected to top $5.0 billion.

Clients who are involved in the DePuy hip recall claim process are encouraged to visit our dedicated website, ASRHipSettlement.com, to understand how they may be able to benefit from a structured settlement should their claim against DePuy result in any monetary compensation.

Clients who are involved in the DePuy hip recall claim process are encouraged to visit our dedicated website, ASRHipSettlement.com, to understand how they may be able to benefit from a structured settlement should their claim against DePuy result in any monetary compensation.

Posted: May 22, 2012 | Category: Articles, Blog, DePuy ASR Hip Recall, Structured Settlements | Comments Off on DePuy Exhibited “Bad Behavior”

Retirement Goggles

Are Your Eyes Open About Your Retirement?

Expanding on the theme of yesterday’s newsletter, “The Secret to Living Well at 100,” which we sent our clients so they can properly plan for their financial futures, here’s some supplemental information you’re sure to find helpful.

Expanding on the theme of yesterday’s newsletter, “The Secret to Living Well at 100,” which we sent our clients so they can properly plan for their financial futures, here’s some supplemental information you’re sure to find helpful.

And probably more than a little disconcerting.

Simply put, we all need to take off the retirement goggles and face some cold, hard facts:

- Most of us DO NOT have enough savings to live the rocking chair retirement we once imagined.

- Many of us WILL live a whole lot longer than we ever believed possible.

- Annuities and pensions are among THE BEST options to protect yourself from the possibility you will become someone else’s financial responsibility later in life. Yet too few people take full advantage of these attractive alternatives.

People anticipating personal injury settlements and the attorneys who represent them are uniquely positioned to fill this retirement reality void by accepting structured settlements and structured attorney fees when their cases settle. Both offer so much potential to lay a strong foundation for a very secure future.

While the appeal of cash when a case settles is understandably very strong, large sums of cash have been known to cause as many problems as they solve. Ask anyone who’s gone through an inheritance dispute. Or many lottery winners.

By contrast, safe, secure, tax-advantaged future cash flows that are GUARANTEED make life so much easier. It may not produce the same “thrill of being rich” (if only for a while) but it gets to the foundation of an injury settlement. Structured settlements address real needs.

Retirement gap bridging is a very real need for almost everybody.

Some excellent recommended further reading from DailyFinance that highlights our concerns for our clients and some of our favorite quotes the articles contain:

“Should You Accept a Pension Buyout Offer?”

” . . . taking the lump sum puts the responsibility of investing on your shoulders.”

” . . . if you make a bad investment, you’ll never get your lost money back.”

“Sometimes, the best answer will be to turn that money down and keep collecting safe, stable monthly checks for the rest of your life.”

“Prepare for a Scary Income Gap in Retirement”

” . . .38% of current retirees don’t generate enough income to cover their expenses and are thus already living on borrowed time.”

“When it comes to retirement funding, ‘hope’ is not a successful strategy.”

Whether you are a soon-to-be retiree considering your options, a personal injury claimant contemplating a settlement offer or a plaintiff attorney looking to solidify your post-legal career financial position, call us to let us help you evaluate your options. We’re committed to helping you meet your long-term financial needs in the safest way possible.

Posted: May 11, 2012 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on Retirement Goggles

The Secret to Living Well at 100

Be Healthy and Have Money

to Live Until Age 100 or Beyond

OK, so it’s not really a “secret” that being healthy and having money are essentials to a comfortable retirement. Pretty obvious actually.

But how prepared are you for the possibility that you just might be a healthy centenarian some day?

What if you live “too long”?

In addition to reading Robert Powell’s MarketWatch column “Planning for retirement? Plan to live to 100,” you may wish to consider these statistics from the Journal of Population Research:

- Life expectancy in classical Greece and Rome was 35 years

- Life expectancy in the Victorian Era was 40 years

- Life expectancy in the 1900s was 73 years

- Life expectancy today is about 84 years

Thanks to improved sanitation, better living conditions, advances in science, not engaging in the carnage of neighboring villages, T-Rex extinction, etc., our life expectancies have improved dramatically over time. Particularly in the past century.

To the north of us in Canada, the Atkinson Fellowship in Public Policy published an interesting and fairly extensive Special Report in 2007 entitled “Ontario braces for a grey wave” that is worth a read for anyone who wants a glimpse of what the future may hold as they age.

To the north of us in Canada, the Atkinson Fellowship in Public Policy published an interesting and fairly extensive Special Report in 2007 entitled “Ontario braces for a grey wave” that is worth a read for anyone who wants a glimpse of what the future may hold as they age.

Boomers’ Biggest Retirement Fears

Last year, US News Money reported the findings of an AARP survey that asked 50-somethings to identify their biggest fears. Not surprisingly, the top two fears of baby boomers were:

- Health care; and,

- Running out of money

Since we’re not experts in offering advice on how to improve your overall physical health, we’ll stick to something we do know a thing or two about: Improving your financial health.

“Pensionize”

If forced to boil a sensible retirement strategy down to its simplest, easiest to implement solution, we would advise anyone who wants to protect themselves against the possibility of living too long to remember one word:

“Pensionization”

“Pensionizing” refers to converting a single lump sum via product allocation into a series of future tax-advantaged cash flows one can never outlive. People, it turns out, like the idea of guaranteed lifetime income as evidenced by the high satisfaction levels of those currently receiving Social Security benefits and traditional pension payments.

And the longer you live, the better the value of your “pensionization” choice and the higher your retirement satisfaction.

Plus, “pensionizing” is a concept that is easy to understand and simple to implement.

The trademarked phrase originated from an excellent book Pensionize Your Nest Egg which analyzes the challenges faced by Canadian retirees and offers some solutions to the population there. We highly recommend this book and hope the authors some day will write a version applicable to the United States.

In our practice, the categories of clients we most frequently help with “pensionizing”are:

- Structured Settlements: Those in the process of settling personal injury claims;

- Structured Attorney Fees: Attorneys representing clients who are settling personal injury claims; and,

- Retirement Fund Roll-Overs: Clients seeking to convert portions of their eligible 401(k) and IRA balances.

With the checks and balances built into the insurance regulatory system today, the safety and security of guaranteed lifetime income from a highly rated life insurer is difficult to replicate.

Even financial professionals who profess to loathe annuities, will admit that a portion of one’s retirement funds should be allocated to annuities as a hedge against a long life.

The National Structured Settlements Trade Association recently blogged about how nicely structured settlements can complement one’s retirement planning.

So whether you are being offered a structured settlement as an option for a personal injury claim, are an attorney looking to sensibly plan for your future or a current or “soon-to-retire” baby boomer tired of the ups and downs of the stock market, call us to let us help you make an informed decision about your future.

Posted: May 10, 2012 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on The Secret to Living Well at 100

Wrongful Convictions Tax Relief Act of 2012

Legislation would provide tax break for the wrongfully convicted

April 19, 2012 – With DNA evidence helping lead the way toward exoneration of those who have been falsely convicted and wrongfully imprisoned, a bill in Congress introduced last month by Congressmen Sam Johnson (R-TX) and John Larson (D-CT), would institute fairness to countless men and women who have suffered indignities.

In short, H.R. 4241 would amend the Tax Code to allow those who win their freedom for crimes they did not commit to receive damage awards on a 100% income tax-free basis. The bill is currently in committee.

A few years ago, I had the privilege of assisting several exonerated prisoners make structured settlement choices for the civil suits they successfully pursued following their release from prison. Fortunately, they had expert legal counsel who advocated vigorously on their behalf to win their freedom.

In each case, these men spent more than a decade in prison for crimes they were ultimately vindicated of. The structured settlements they selected enabled them to lay the foundation for a financially secure future and helped them, to the extent possible, move past their negative experiences of being incarcerated for something they didn’t do.

Financial security after maximum security gave them peace of mind they hadn’t know in years.

So inspired was I by my experience in helping these men, I joined the Board of Directors for Innocence Matters, a California nonprofit dedicated to helping prevent wrongful convictions through education, prevention and reform.

Finn Financial Group resoundingly applauds Reps. Johnson and Larson for their courage in recognizing the disparity that exists in taxation of damages for this important class of Americans whose liberties were denied them and urges the bill’s passage.

For an excellent analysis of this matter, some historical perspective and the existing challenges giving rise to the need for this bill, we recommend the March 30, 2012 edition of Tax Alert by renowned taxation of damages tax attorney Robert W. Wood.

Posted: April 18, 2012 | Category: Articles, Blog, Structured Settlements | Comments Off on Wrongful Convictions Tax Relief Act of 2012

Finns with Faulty Hip Implants

April 10, 2012 – Sometimes, you just need to let the headline do the talking. Case in point from today’s International Edition of Scandinavia’s largest subscription-based newspaper, Helsingin Sanomat:

“Thousands of Finns may have faulty hip implants”

To view a short video about one particular “Finn” who underwent bilateral hip replacement surgery and understands, go to:

If you think you will receive compensation for injuries stemming from a faulty implant device, you are wise to educate yourself about the benefits of structured settlements well in advance of finalizing any settlement.

Please call to let us know how we can help you. We look forward to helping you secure a portion of your financial future.

Posted: April 10, 2012 | Category: Articles, Blog, DePuy ASR Hip Recall, Structured Settlements | Comments Off on Finns with Faulty Hip Implants

Consumer Reports: Artificial hips never tested

Recalled DePuy ASR hips among devices untested

March 29, 2012 – In its upcoming May edition, Consumer Reports presents the results of its investigation which calls into question the current process of medical device regulation that their advocacy wing, Consumers Union, believes fails to “protect patients from harm.”

Entitled “CR Investigates: Dangerous medical devices,” CR sheds light on the process involved in bringing medical devices to market in the United States.

For those specifically interested in the now-recalled DePuy ASR artificial hip implants, the report features compelling testimony from an orthopedic surgeon who personally suffered from the ill-effects of the DePuy ASR hip implant device. Stephen Tower, MD was “injured by the same artificial hip he implanted in patients.”

A number of lawsuits have unfolded as a result of allegations that the DePuy ASR hip implant devices were defective. Litigation is ongoing and our firm remains committed to following this matter closely as it progresses.

Patients who may eventually be anticipating negotiated settlements stemming from their lawsuits are encouraged to familiarize themselves with the advantages of settling with a structured settlement. To watch a brief video on the topic, please visit our firm’s sister site at:

Call us for additional information about the advantages of settling your lawsuit with a structured settlement. Our free consultations are designed to help you make an informed choice about your financial future.

Posted: March 29, 2012 | Category: Articles, Blog, DePuy ASR Hip Recall, Structured Settlements | Comments Off on Consumer Reports: Artificial hips never tested

College Affordability Improves

“I believe that we parents must encourage our children to become educated, so they can get into a good college we cannot afford.”

– Dave Barry –

In a classic example of supply-and-demand and in response to the realities of an economy that has left many people lacking the wherewithal to meet the post-secondary educational needs of their offspring, some colleges are getting creative in an effort to attract more students.

In his article “Colleges slashing tuition, offering 3-year degrees,” columnist Blake Ellis, writing for CNNMoney, cites examples of the “extreme measures” some institutions of higher learning are taking to increase the student body head count. Among them:

In his article “Colleges slashing tuition, offering 3-year degrees,” columnist Blake Ellis, writing for CNNMoney, cites examples of the “extreme measures” some institutions of higher learning are taking to increase the student body head count. Among them:

-

Cutting tuition by double digits

-

Freezing tuition hikes

-

Offering three-year degree programs

-

Offiering four-year graduation guarantees

While not all halls of ivy are embracing this approach to making a college degree more affordable, this is certainly welcome news for anyone looking to pursue higher education.

Those settling personal injury claims frequently arrange to have their settlement proceeds paid via a structured settlement designed to coincide with anticipated college costs for themselves, their children or grandchildren.

Posted: March 22, 2012 | Category: Articles, Blog, Structured Settlements | Comments Off on College Affordability Improves

Pro-Bowl QB Facing Financial Ruin

Mark Brunell’s Career Earnings of $50 Million . . . Gone!

March 9, 2012 – With the NFL Scouting Combine recently concluded and Draft Day fast approaching, many college football players, no doubt giddy with anticipation, will soon be eagerly awaiting that life-changing phone call from an NFL team which will hopefully set them on the path to stardom and financial independence.

A select few will sign contracts worth millions upon millions of dollars they could only dream about only a few years earlier.

Many more will sign less bountiful, but still very lucrative, contracts commensurate with their talent and market value.

The lucky ones who remain healthy will parlay their talent into long NFL careers that will pay them an accumulated sum of money designed to ensure a lifetime of prosperity.

But for one such player who has “been there, done that,” the end result is shaping up to be far different than planned.

According to “Jets Quarterback Mark Brunell’s Catastrophic Financial Path,” the three-time Pro Bowler “blew all his money with lousy investments into nine businesses.” Bankruptcy court filings reveal his plans to begin a $60,000 per year job as a medical sales rep once his playing days come to an end.

By all accounts, Mark Brunell is a great guy with a heart of gold and tremendous work ethic. But his tale of woe is proof that neither these qualities nor athletic prowess on the gridiron assures anyone success with money matters.

Problem Not Isolated to NFL Players

Even though a disproportionately high percentage of former NFL players end up “bankrupt, divorced or unemployed” according to ex-Green Bay Packer Ken Ruettgers who helps retired players who are down and out, the problem is not unique to this demographic.

A comprehensive study of personal injury plaintiffs who reject structured settlement offers and accept cash settlements instead does not exist; however, stories about people who spend their settlements faster than anticipated abound.

Mark Brunell’s story is certainly not a happy one. But at least he is young and can yet recover from his misfortune. When plaintiffs are anticipating large personal injury settlements, it’s usually because their ability to support themselves in the future has been seriously compromised.

They cannot afford to take risks!

For this reason, a structured settlement should serve as the foundation of any individual’s post-settlement financial planning strategy. It affords them the BEST opportunity to cost-effectively guarantee they will not outlive their money and end up penniless.

In its pamphlet, “Structured Settlements: Your Future. Guaranteed,” the National Structured Settlements Trade Association highlights several of the unique advantages structured settlements offer.

Retirees, Too, Benefit From Lifetime Income

In addition to personal injury plaintiffs, soon-to-be retirees looking to convert their life savings into guaranteed, secure cash flows should look to lifetime annuities which are the most cost-effective and least risky asset class for generating guaranteed retirement income for life, according to the scholarly work of two Fellows of the Wharton Financial Institutions Center in their article Rational Decumulation.

Let Us Help

Whether you’re in need of structured settlement expertise or seeking to roll-over your 401(k) or IRA, we can help. As specialists in offering financial solutions with your long-term financial security in mind, we’re here to help.

Thank you for the opportunity to be of service!

Posted: March 9, 2012 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on Pro-Bowl QB Facing Financial Ruin

FDA Warned DePuy of ASR Hip Problems

A Full Year Before World Wide Recall

The New York Times reports that an executive for DePuy Orthopaedics, a subsidiary of Johnson & Johnson, sent an email to top executives of the company about the U. S. Food and Drug Administration’s unwillingness to approve one of the metal-on-metal artificial hips it manufactured because “a significant number of revisions” were needed compared to a control group.

DePuy ASR artificial hips were recalled in August of 2010.

Despite DePuy’s offer of assistance to patients impacted by the recall (they have an entire website dedicated to the effort), attorneys around the country have filed lawsuits against the medical device maker.

Our firm is uniquely positioned to serve as a resource to patients affected by the DePuy ASR recall and the attorneys who represent them. For an informational video on why our firm is following this news so closely and to learn how we may be able to help, please visit:

We continue to monitor this on-going situation and look forward to being of service. Please let us know how we can help you.

Posted: February 26, 2012 | Category: Articles, Blog, DePuy ASR Hip Recall, Structured Settlements | Comments Off on FDA Warned DePuy of ASR Hip Problems

NYT: DePuy Recall Leads to $3 Billion Charge for Parent Company

January 25, 2012 – Johnson & Johnson, parent company of DePuy Orthopedics, maker of the since recalled metal-on-metal ASR artificial hip systems, recently took quarterly charges of more than $3.0 Billion according to the New York Times.

As a structured settlement company with a personal interest in the litigation that has developed in light of problems associated with certain artificial hips, we have great interest in assisting those who are pursuing legal remedy for products liability lawsuits stemming from the hip recall.

For those affected, we have established a special website dedicated to the matter and encourage all prospective clients and their representatives to visit us there. Please visit:

We continue to follow the DePuy hip recall matter with great personal and professional interest and look forward to being of service to you. Please let us know how we can help.

Posted: January 25, 2012 | Category: Articles, Blog, DePuy ASR Hip Recall, Structured Settlements | Comments Off on NYT: DePuy Recall Leads to $3 Billion Charge for Parent Company