Structured Settlements Looking Up

January 6, 2014 – Structured settlements were created to specifically help address the long term financial needs of those settling personal, physical injury claims.

Because injury settlement proceeds represent neither savings nor investment dollars, comparing their returns to other “investments” can be a dangerous method of evaluating their imporatance to someone who can’t risk losing money.

This helps explain why structured settlements have remained an extremely popular cash settlement alternative for decades even though rates fluctuate.

After all, what’s not to like about something that is:

100% income tax-free (principal and interest);

tailored to one’s unique set of circumstances;

safe, secure and guaranteed by highly rated companies?

Yet, even though they are not investments per se, like the kids in the AT&T commercial who intuitively understand that “more is better,” everybody prefers higher payouts to lower ones, everything else being equal.

For this reason, we’re happy to report that a recent financial barrier was eclipsed as America was gearing up to change calendars in late December.

The 10-years Treasury closed above the psychologically important 3.0% threshold for the first time in more than two-and-a-half years.

The 10-years Treasury closed above the psychologically important 3.0% threshold for the first time in more than two-and-a-half years.

While investors don’t cheer when bond rates rise, those looking for long-term financial security do.

What’s this got to do with structured settlements?

As one of our life company partners communicated on Friday:

“Higher rates will make our structured settlement products even more attractive as we begin the new year.”

So if you’ve been on the sidelines for the past few years assuming that “structured settlement rates are too low,” make this the year you resolve to jump back in.

Whether you are a claims representative or plaintiff attorney negotiating an injury settlement, DON’T ASSUME rates are “too low” for you to consider.

Incorporating a structured settlement into an overall claim resolution is a proven strategy that can add much value to the settlement process and much security to the injured person.

Best wishes for a healthful and prosperous 2014!

Posted: January 6, 2014 | Category: Articles, Blog, Structured Settlements | Comments Off on Structured Settlements Looking Up

2014 Financial Resolutions Study

December 31, 2013 – According to the recently published Fidelity 2014 New Year Financial Resolutions Study, 54% of you are making financial resolutions for the coming year.

While we can’t help you save more, spend less or pay down debt – the top three financial resolutions cited in the study – there are two specific areas where we CAN help you take command of your own financial future.

Retirement Annuities

Retirement account balances have rebounded, America is getting older and nobody wants to risk losing money again as happened to many during the Great Recession.

Add to this the fact that people are happier and feel more secure when they know they are receiving guaranteed lifetime income and the stage is perfectly set for a conversion of some of those ear-marked funds to a lifetime annuity.

Through the first nine months of 2013, $167.6 billion worth of annuities were purchased according to Life Insurance Marketing and Research Association (LIMRA).

While every annuity channel experienced increased activity, we concentrate on helping clients with low-to-moderate risk tolerance with their Fixed Annuity and Indexed Annuity choices to meet their retirement planning needs.

Structured Attorney Fees

Contingency fee-based attorneys have a unique opportunity to defer recognition of earned fees into a future year for a distinct tax advantage.

So strongly do we believe in this popular money-saving strategy which accounts for about 25% or more of our business in any given year that we maintain a companion website dedicated to the topic:

And even though she wasn’t specifically talking about structured attorney fees, InvestmentNews columnist Darla Mercado helps illustrate the case for this option in today’s article “Getting a jumpstart on 2014 tax planning” by urging . . .

” . . . certain high earners might want to manage their income stream in order to keep themselves from drifting into higher tax brackets.”

So if your New Year’s resolution involves securing your financial future, we hope you’ll give us an opportunity to show you how we may be able to help you achieve your goals.

Posted: December 31, 2013 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on 2014 Financial Resolutions Study

2014 Poised To Be “The Year of The Annuity”

December 23, 2013 – It’s always nice to read something that gives you reason for optimism as you prepare to change calendars and head into a new year.

An article in today’s InvestmentNews caught our eye because it predicts 2014 could “be a big one” for a certain financial option near and dear to our firm’s heart.

“New year could bring a boon for annuities,” points toward a growing appreciation for this powerful, if historically under-appreciated, financial security solution.

If you’ve felt completely clueless about what an annuity is or how you can benefit from owning one up to this point in your life, fear not.

You are not alone.

Because 70% of the public cannot correctly define an annuity, the Insurance Information Institute produced this 2-minute video as a public service to help fill the educational void:

All this lack of knowledge is changing, though, as built up demand for safe, secure cash flow options increases.

People want safety and security and many are more than a little risk averse.

As specialty annuity specialists (say that three times fast!), we are focused on helping people secure their financial futures through the effective use of specialty annuity products and services tailored to their unique needs.

While structured settlements remain the foundation of our business, we have experienced a major increase in requests from long term clients seeking assistance in converting their retirement savings into a “personal pension” so they never have to worry about outliving their money.

Part and parcel to this long-term retirement planning focus has been the significant increase in requests from plaintiff attorneys desiring to structure their fees. In fact, 2013 was our best year ever in this area as tax brackets have risen.

So if one of your New Year’s resolutions is to take charge of your own retirement, let us show you how we have helped so many others.

2014 may be the Year of the Horse according to Chinese zodiac, but right here we’ll also be celebrating the Year of the Annuity.

2014 may be the Year of the Horse according to Chinese zodiac, but right here we’ll also be celebrating the Year of the Annuity.

You are most welcome to join the celebration with us! Call anytime we can help.

Best wishes for a very, Merry Christmas and a Happy and Prosperous New Year.

Posted: December 23, 2013 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on 2014 Poised To Be “The Year of The Annuity”

Locking in Your Gains . . . For Life

December 5, 2013 – If you’re among the lucky ones, you had some retirement money saved up in your 401(k) or IRA in 2008, lost a bunch of it in the ensuing Great Recession years, gutted it out through 2013 and now have recovered most, if not all, of the wealth you originally watched evaporate.

If you were even luckier, you stayed invested and maybe even continued to make contributions to the market and are now comfortably ahead of where you were back then.

So now what?

My choice of gambling oriented words like “lucky” and “luckier” in the first two paragraphs is not accidental. The market is, after all, a crap shoot which goes up some years and goes down others even if the longer term direction trends positive.

My choice of gambling oriented words like “lucky” and “luckier” in the first two paragraphs is not accidental. The market is, after all, a crap shoot which goes up some years and goes down others even if the longer term direction trends positive.

But nobody, and I mean NOBODY, really knows what the market will do in the future despite the availability of exhaustive data and the existence of many sound strategies designed to help “hedge your bets” if you do choose to stay in the market.

Because negative years in the stock market, when experienced closer to retirement, can disproportionately and detrimentally impact one’s chances for retirement security and happiness, many people look for safer alternatives to simplify their golden years.

Enter deferred-income annuities

Earlier this week, under the broad heading of “Best New Money Ideas,” CNNMoney featured six “Best new ways to make money” as we head into 2014.

According to the authors, one the “Best new investment ideas” is also the “Best new retirement tool . . . ”

We haven’t seen the word “Best” featured so prominently in an article since the August 23, 1962 issue of Mersey Beat when The Beatles announced Ringo was joining the band as its new drummer.

We haven’t seen the word “Best” featured so prominently in an article since the August 23, 1962 issue of Mersey Beat when The Beatles announced Ringo was joining the band as its new drummer.

And NEVER In a financial column.

(Emphasis on Best is ours throughout, btw)

The CNNMoney piece describes an excellent retirement strategy, growing exponentially in popularity, designed to ensure you don’t end up broke in your later years.

With life expectancies ever-increasing, designating a portion of your retirement assets NOW to guarantee lifetime income in the FUTURE is one of the Best things you can do to secure your future.

And it’s not just easy, it makes financial sense:

“lifetime annuities are . . . the most cost effective and least risky asset class for generating guaranteed retirement income for life.”

– Economists David F. Babbell and Craig B. Merril –

I hope you’ll take a few moments to read the helpful CNNMoney column.

Then give us a call. We’ll provide you with several preliminary quotes and we’ll walk you through the rest if you decide this option makes sense for you.

We like helping make people happy and helping them secure their financial futures.

You might even say it’s what we do Best.

Posted: December 5, 2013 | Category: Articles, Blog, Retirement, Structured Settlements | Comments Off on Locking in Your Gains . . . For Life

November 22, 1963 Reflections

November 22, 2013 – Average life expectancy at birth being what it was in pre-war America, it’s a sobering reality that a significant percentage of Americans who were adults aged 30 and older in 1963 are no longer around to share their “I remember the day President Kennedy was shot” stories with us.

In another 20 years or so, all of them will likely be gone.

So the story-telling will ultimately fall to those of us who were just kids on that tragic day to share our reflections until, by the 100th anniversary of Kennedy’s assassination, no one will be left to talk about what they remembered.

And given a kid’s natural lack of appreciation for the true significance of current events as they occur, I hope any insensitivity of our perceptions will be forgiven.

My Story

I can’t actually remember whether or not it was preceded by a P.A. announcement but sometime in the middle of the afternoon, not long after lunch and shortly before we would leave school for the weekend, Sr. Marlene told us President Kennedy had been shot.

can’t actually remember whether or not it was preceded by a P.A. announcement but sometime in the middle of the afternoon, not long after lunch and shortly before we would leave school for the weekend, Sr. Marlene told us President Kennedy had been shot.

Because we all wanted to help him get well, we were instructed to get out of our desks to kneel and pray for his recovery.

President Kennedy was, after all, the second most important Catholic in the world after the Pope.

At Holy Family, we had kneeled by our desks in prayer before. A rote exercise, like saying the Pledge of Allegiance, our regular prayers were part of our morning routine if we didn’t have Mass. Usually, though, it was not much more than a quick Hail Mary and maybe a Glory Be or two. Kneeling for a bit wasn’t a big deal.

But this day would be different.

Whether the floors were hardwood, tile, terrazzo or whatever they make anvils out of, I can’t recall. I can only tell you that people were not meant to kneel for extended periods of time on hard surfaces.

Maybe this kind of thing was de rigueur in the Middle Ages but it certainly wasn’t cutting it in 1963. At least not for me.

If the president would just hurry up and get better, we could get back in our seats. What was taking so long? Why wasn’t this working? My knees hurt!

We weren’t allowed to talk but, wondering if my classmates were equally discomforted by this cruel rite that went on for the better part of an hour if not longer, I turned toward my friend John Bodnark when Sr. Marlene wasn’t looking to see how he was holding up.

His expressive look of disbelief was only slightly reassuring that someone else felt the same as I. He mimed that he was kneeling on his fingers every so often to disperse some of the weight. Not a bad idea. I tried it. It helped and I was grateful.

Over on the other side of the aisle, Joni Baugh, the apple of my second grade eye, was downright stoic. Angelic in her sincerity with eyes closed, head bowed piously and mouthing devotions with the conviction of a saint, I was only too aware that girls just seemed to be better equipped to handle this kind of thing.

With mixed emotions of agitation and relief, we were finally allowed to board the school buses for home still believing the president was in the hospital. We may have even been sent home early. I don’t remember.

Walking through our back door by way of the garage that day (nobody used their front doors except to greet delivery people and company), my mom was waiting in the kitchen to meet my older brother and me when we arrived home from school.

“Do you know what happened today?” she asked not even bothering to find out how our day was as she usually did.

“Someone shot the president,” I responded matter of factly. “Is he okay?”

That’s how I learned John F. Kennedy was dead. My mom told me in our kitchen.

The nuns must have known by the time we left school that JFK was dead but wanted our parents to tell us the news I’m pretty sure. Probably a good call.

My mom’s delivery of the news was pretty steady. However traumatized she may have been inside, she probably didn’t want to upset her boys so she kept her emotions in check.

While this news surprised me a little bit because it never occurred to me that the president would actually die, everything in my house still looked the same so I just assumed everything would go on as usual.

I went to change out of my school uniform into my play clothes shrugging off the news of one of the seminal moments in world history.

Thanksgiving was next week and my birthday was coming up in a few days on the 25th, a birthday I shared with my baby brother, Dennis, who would be turning two and the president’s son, John-John, who would be celebrating his third birthday. I was going to be eight.

Wonder what kind of presents I would get?

The next morning was when the gravity of the situation hit me personally and really made me sit up and take notice of what was going on.

Where were the cartoons?

Every single television station, all three of them, had continuous coverage of nothing but old people talking and walking around in overcoats.

Whoever heard of a Saturday morning without cartoons?

I wanted Beany and Cecil, Quick Draw McGraw, Bugs Bunny and the rest of my regular Saturday morning pals but all I got was the drone of people talking about the same thing and no amount of protesting and complaining was going to change my weekend reality.

“You watch this. You’ll never see anything like this again as long as you live,” my dad insisted.

It would be many years before I fully appreciated how right he was.

The next day when Oswald was shot, I assumed everyone would be happy. After all, in the movies, when bad guys were shot, it was a good thing.

Wasn’t this the way it was supposed to be?

This is why I was so surprised to discover my mom talking to someone on the phone, probably her mom, late that Sunday afternoon crying because Oswald had been killed.

“First Kennedy and now Oswald,” she sobbed. “What’s this world coming to? What next?”

No comforting answers would be forthcoming.

Now I was really confused though. My mom never cried when Kennedy was shot but she cried when Oswald died? Why wasn’t she happy about this? After all, he was the bad guy, right?

As the weekend drew to a close, my final Kennedy remembrance was that of my dad and family friend Henry Withers watching the news coverage of Oswald’s assassination in our living room.

“Look at him. He’s just waitin’ for it. He knows it’s coming,” Henry insisted, an early devotee of the conspiracy theory that casts Jack Ruby as the hired gun sent to silence Oswald.

Henry and my dad spent the rest of Sunday evening drinking and debating what really happened that fateful weekend.

Within the year, our family would relocate to another city causing me to leave behind friendships that would never fully develop but paving the way for many others that never would have been.

Both events were early, if harsh, lessons that life always goes on.

Tragic events often cause people to make decisions they might not otherwise make so who knows if the Kennedy assassination had anything to do with my parents’ decision to relocate back the city where their own parents still lived.

I just know that fifty years later, people are still debating what happened in Dallas on November 22, 1963.

And even if a lot of them are doing so online instead of sitting in living rooms together, such a shared experience connects us all regardless of our backgrounds.

A few of us are even still around who can still say “I remember the day President Kennedy was shot.”

Now if only we were sure we knew the whole truth.

Posted: November 21, 2013 | Category: Articles, Blog | Comments Off on November 22, 1963 Reflections

Retired Claims Adjuster is Top JFK Assassination Researcher

November 21, 2013 – My dad was a claims adjuster.

Thirty years ago, I began my insurance career as claims adjuster.

My wife, too, was a claims adjuster. We met at work.

One of my brothers was a claims adjuster.

So was his godfather.

All told, my family and our assorted godparents can lay claim (pun intended) to about 150 years of adjusting and insurance experience.

So when, while reading an article entitled “One JFK conspiracy theory that could be true,” I learned that one of the world’s preeminent Kennedy assassination researchers is a retired claims adjuster, I knew this was a guy whose opinion I was going to value.

Dave Perry doesn’t so much set out to prove conspiracy theories as he does to rule out why they can’t be true using simple, good old-fashioned fact verification techniques.

Dave Perry doesn’t so much set out to prove conspiracy theories as he does to rule out why they can’t be true using simple, good old-fashioned fact verification techniques.

Not unlike a claims adjuster who uncovers an original receipt for an item on a theft inventory for which the insured estimated a different figure, he values only the verifiable.

The world will likely never be satisfied with the Warren Commission report or any of the subsequent theories of “Who Really Killed JFK?”

But with a professionally trained insurance adjuster looking into things, we can at least take comfort in knowing every possible (dare I say, Oliver) Stone is being unturned.

Posted: November 21, 2013 | Category: Articles, Blog | Comments Off on Retired Claims Adjuster is Top JFK Assassination Researcher

Structured Settlements vs. Stocks

November 20, 2013 – It’s too bad Las Vegas isn’t taking bets on this hypothetical match-up: Structured settlements vs. stocks.

I’m not much of a gambler myself but if I were and they were, I’d put a whole lot of money on structured settlements coming out on top.

And if yesterday’s CNNMoney article, “Welcome to the 4% return market” is any indication, I wouldn’t be alone since “among a growing group of forecasters, 4% is becoming something of a consensus.”

And if yesterday’s CNNMoney article, “Welcome to the 4% return market” is any indication, I wouldn’t be alone since “among a growing group of forecasters, 4% is becoming something of a consensus.”

If you don’t want to read the short article yourself, here’s one of the major take aways:

Since The Great Depression, stocks have risen just 4% a year in the decade following a market where P/E ratios have traded where they are now.

But we’d like to remind you: When stocks are cashed out, taxes are due on the gain whereas structured settlement payouts stemming from a personal, physical injury claim are paid 100% income tax-free.

In other words, the experts are predicting that the best case scenario for stocks is right about where tax equivalent yields for structured settlements are right now.

So we can’t help wondering:

Who would willingly risk being on the losing end of a bet whose best case scenario equals the guaranteed sure thing?

The worst case scenario for stocks, of course, is something like 2009 all over again even if that scenario seems unlikely. In poker, they’d call that hand a bust.

So even though nobody’s actually taking bets on the imaginary structured settlement vs. stocks card, we’ve got our phantom money riding on structured settlements all the way.

Every situation is unique, of course, but those who choose the tried and true method of resolving their personal injury claim with a structured settlement always leave the tables with money in their pockets.

And that’s the closest thing to a sure bet as you’re ever likely to see.

Posted: November 20, 2013 | Category: Articles, Blog, Structured Settlements | Comments Off on Structured Settlements vs. Stocks

2 Steps To A Happier Life

Click on the Smiley Face . . .

. . . to be transferred to our November 15, 2013 newsletter where you can learn about two choices you can make that are scientifically proven to make you happier.

Posted: November 19, 2013 | Category: Articles, Blog, Newsletter, Retirement, Structured Settlements | Comments Off on 2 Steps To A Happier Life

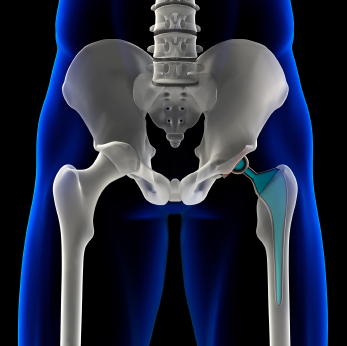

DePuy Hip Lawsuit Settlement

November 13, 2013 – Rumors began circulating this afternoon that Johnson & Johnson has agreed to a $4.0 billion products liability settlement to end the litigation of more than 7,500 pending lawsuits in state and federal courts, alleging metal-on-metal artificial hips, manufactured be subsidiary DePuy Orthopaedics, were defective.

November 13, 2013 – Rumors began circulating this afternoon that Johnson & Johnson has agreed to a $4.0 billion products liability settlement to end the litigation of more than 7,500 pending lawsuits in state and federal courts, alleging metal-on-metal artificial hips, manufactured be subsidiary DePuy Orthopaedics, were defective.

If this turns out to be true then we weren’t far off on our prediction a few days ago that such a settlement was nigh. In a game of horseshoes, this would have been called a “leaner” worth two points.

We’ll remained focused on the details of this settlement with great interest (assuming it pans out) as it unfolds over the course of the coming weeks and months and stand ready to assist anyone who can benefit from the unique advantages structured settlements afford them in this type of litigation.

NOTE: It’s important to stress at this time that the terms of any settlement are said to be confidential so any reports, including this one, should be considered unofficial.

For additional information on how you can benefit from structuring your DePuy hip settlement, please visit our companion website dedicated to this unique class of plaintiffs to learn how we can help and why we feel so strongly about this particular group of lawsuits.

Visit: ASRHipSettlement.com

Thank you for the opportunity to be of service!

Posted: November 13, 2013 | Category: Articles, Blog, DePuy ASR Hip Recall, Structured Settlements | Comments Off on DePuy Hip Lawsuit Settlement

DePuy Hip Recall & Tea Leaves

November 7, 2013 – When you follow large, complex class action or mass tort products liability litigation matters, as we have been doing for several years with the DePuy ASR artificial hip lawsuits, it’s hard to predict with any degree of accuracy when things are finally going to end.

But there are signs that things could be coming to a femoral head on this litigation in the not-too-distant future.

From the March, 2009 filing of the first products liability lawsuit against DePuy alleging its ASR artificial hips were defective;

Through the August, 2010 worldwide recall of the device by DePuy Orthopaedics;

Through the August, 2010 worldwide recall of the device by DePuy Orthopaedics;

Through the December, 2010 multidistrict litigation (MDL) consolidation of a number of cases in Northern Ohio;

Through the $8.35 million verdict in Los Angeles – Kransky v. DePuy Orthopaedics, Inc. – in March, 2013;

Through a couple of recent postponements of several bellwether cases scheduled to begin this year and ongoing rumblings that Johnson & Johnson, DePuy’s parent company, has been weighing a $3.0 billion offer to settle more than 11,000 of the pending lawsuits;

Our firm has been monitoring this matter with great personal and professional interest.

And while we’re not taking any wagers on the matter, our tea leaves are leading us to believe this matter could be on the cusp of resolving.

If and when any plaintiffs involved in the DePuy ASR hip litigation do find themselves anticipating any settlements, we hope they’ll let us talk to them about the benefits of structuring their settlement.

We understand. We listen. We care.

That’s why three years ago we created a special companion website

to demonstrate to clients why this litigation is so personal to this firm.

We want to make sure everybody involved is aware of their settlement options and how we can help.

So please take a few minutes to watch our video and let us know what questions you have. We look forward to being of service.

And if the litigation resolves later rather than sooner, that’s OK. Just call us when it does. We’ll still be here to help you.