Dear Congress: This is Wrong!

August 6, 2018 – When the Tax Cuts and Jobs Act, as it’s known, went into effect earlier this year, many hailed the legislation for simplifying things and saving the average taxpayer money.

Others protested the legislation disproportionately benefits the ultra-wealthy who didn’t need and weren’t asking to have their taxes reduced.

Whichever side of the debate you happen to fall on, one category of taxpayers stands out as being most unfairly and adversely impacted by this legislation:

People who hire legal counsel for nonphysical injury claims.

That’s because, whether intentional or inadvertent, Congress failed to consider one disastrous consequence of the new law:

Going forward, taxpayers can no longer deduct attorney fees they incur for many types of nonphysical injury disputes they bring against their alleged tortfeasors.

In an ironic twist worthy of a Shakespearean drama, plaintiffs who “win” their personal, nonphysical injury lawsuits ultimately find themselves on the losing end of their own litigation come tax time.

In an ironic twist worthy of a Shakespearean drama, plaintiffs who “win” their personal, nonphysical injury lawsuits ultimately find themselves on the losing end of their own litigation come tax time.

This careless, shortsighted, unwise and downright mean oversight must be corrected.

Untenable

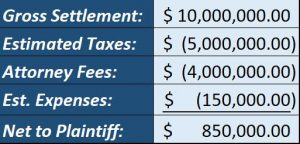

To illustrate how unfair this law, if left unamended, can be, assume Plaintiff A successfully resolves a libel (nonphysical injury) case against Defendant B, pre-trial, for $10,000,000.00. Because the plaintiff is taxed on the ENTIRE award (including attorney fees), the full ten million dollars is considered taxable income.

In California, the tax on this settlement is approximately 49% (married filing jointly) to 50% (single taxpayer), or, roughly $5,000,000.00.

Further assume, since the case was heading to trial, a 40% contingency fee agreement was in place for legal representation – a standard arrangement given the skill required and the financial risk of trial absorbed by the law firm.

Not counting additional costs associated with developing and trying the case which need to be reimbursed and could erode the total recovery further, the plaintiff stands to net a mere 10% OR LESS of this otherwise substantial settlement.

Is it fair that a plaintiff ends up with less than $1,000,000 of a $10,000,000 settlement?

“Let me tell you how it will be,

There’s one for you, nineteen for me”

In some cases where costs are exceptionally high, it’s not inconceivable a plaintiff might end up OWING money on a case they supposedly won!

If the whole point of the litigation process is to right a perceived wrong, to attempt to make someone whole again and to achieve justice, what reasonable person can find anything just about this outcome?

Unconscionable

Remember that $4,000,000 attorney fee? Even though that sum was already considered taxable income to the plaintiff, the attorney who earns and actually receives that money will owe taxes on it as well resulting in the same money being taxed twice!

“Should five percent appear too small,

Be thankful I don’t take it all”

What about the legal fees incurred by the defense? Most likely the defense can deduct their defense costs depending on the type of lawsuit and the status of the defendant.

Add it all up and there is nothing equitable about any of this.

Taxing an individual on money that isn’t theirs and which gets taxed a second time is, at best, a gross failure of the framers of the tax laws to recognize this parity gaffe. At worst, it’s their calculated effort to discourage litigation and allow egregious, harmful behavior to continue unencumbered.

(The irony here, of course, is that plaintiffs now have greater incentive to reject otherwise reasonable settlement offers and proceed all the way through trial. Why not?)

Some exceptions and a partial solution

There are some exceptions to this inability to deduct of attorney fees from the outcome of a nonphysical injury lawsuits.

Most employment and whistleblower cases still permit an above the line deduction for attorney fees as do sexual harassment cases not covered under a nondisclosure agreement. Certain damages, if attributable to one’s business, may also be deductible. Clients are always urged to seek qualified, independent tax advice to analyze their own situation.

NOTE: Income received on account of personal, physical injuries or illness remains tax-free to the plaintiff. Since these damages are not considered income, the attorney fees associated with them are also not subject to taxation to the plaintiff.

Fortunately, much of the headache that accompanies the grievous tax pain can be mitigated by choosing a Nonphysical Injury Structured Settlement during the litigation resolution process. By arranging to have portions of the taxable settlement or verdict paid out over time, a more tax efficient outcome can usually be achieved saving the plaintiff significant sums of money along the way.

While nonphysical injury structured settlements can help ease the tax-induced misery caused by this harmful change in the law, the root of the problem remains. Clients and fair-minded advocates everywhere should voice their concerns to their elected officials lest they someday find themselves on the losing end of a winning proposition.

“Taxman” song lyrics by George Harrison

Taxes gauge image courtesy of Stuart Miles at FreeDigitalPhotos.net